Cyber Security News Aggregator

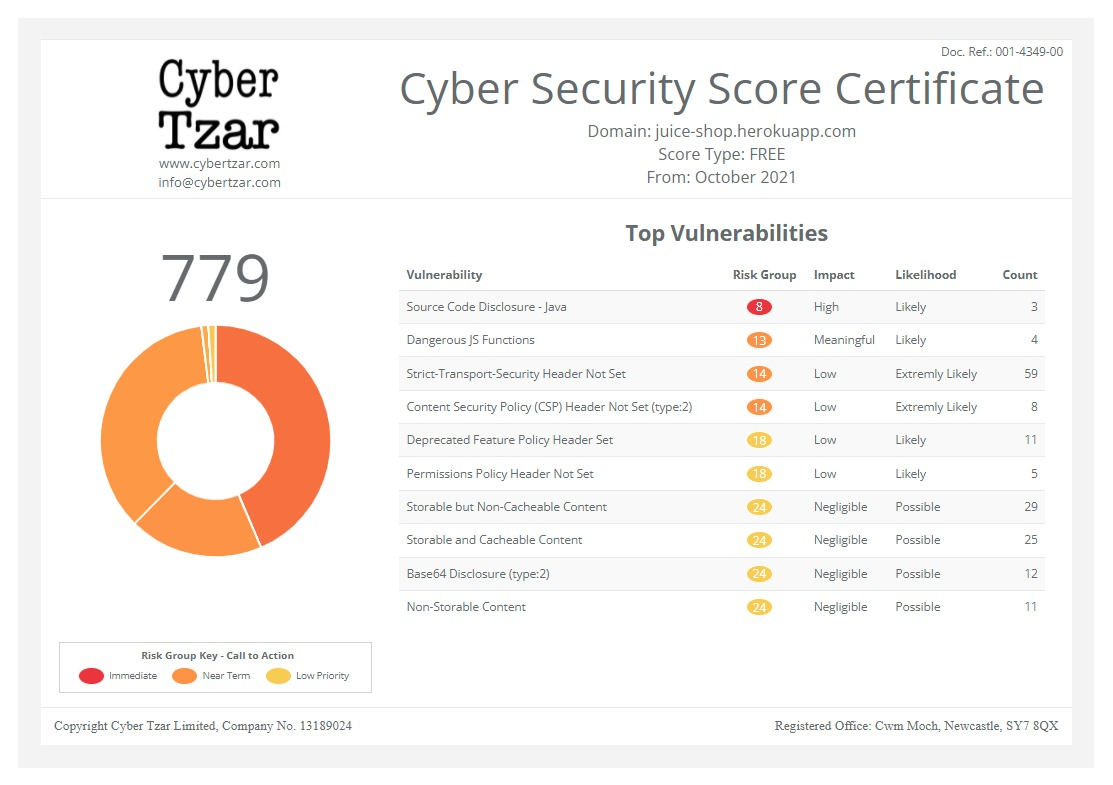

.Cyber Tzar

provide acyber security risk management

platform; including automated penetration tests and risk assesments culminating in a "cyber risk score" out of 1,000, just like a credit score.

First slide label

Some representative placeholder content for the first slide.

Second slide label

Some representative placeholder content for the second slide.

Third slide label

Some representative placeholder content for the third slide.

Does your Cyber Insurance Policy really cover a Cyber Attack?

published on 2023-06-06 11:07:16 UTC by Jared ThompsonContent:

Ensure your cyber security insurance policy does not fall foul of these myths

Regardless of the size of a business, whether you are a sole trader/freelancer or run a thriving business of 100+ employees, it is becoming increasingly essential to have cyber security insurance in place to aid in the recovery process should you ever find yourself a victim.

However, understanding your policy and its requirements is more important than this. Recent trends show businesses rely on their insurance as a be-all-end-all fix when they are the victim of an attack, only to find out they do not meet the policy requirements and receive no remuneration. So read on to avoid these myths about cyber security insurance policies.

- Cyber insurance covers all cyber risks

- Cyber insurance eliminates the need for cyber security measure

- Cyber insurance guarantees full recovery from cyber attacks

- Cyber insurance is only necessary for large organisations

- Cyber insurance is too expensive

Myth 1 - A Cyber Insurance Policy covers all cyber risks

One common misconception is that cyber insurance provides comprehensive coverage for all cyber risks. In reality, policies vary significantly in terms of scope and exclusions. In addition, certain risks, such as reputational damage or loss of intellectual property, may not be covered by some policies. Therefore, reviewing the policy details and carefully understanding the coverage limitations is crucial.

Example:

A small ,retail business assumes its cyber insurance policy will cover any financial losses from a data breach. Still, they later discovered that the policy excludes coverage for payment card industry (PCI-DSS) fines and penalties, which they incurred due to non-compliance with security standards.

Myth 2 - Cyber Insurance eliminates the need for cyber security measures

Some organisations mistakenly believe that having cyber insurance eliminates the need for implementing robust cyber security measures. However, insurance is not a substitute for proper security practices. Insurers often require policyholders to have reasonable security measures, and non-compliance could result in coverage exclusions.

Having a cyber security insurance policy in place is not an excuse or reason not to also implement foundational defences such as strong passwords, password managers, Multi-Factor Authentication, regular backups, anti-virus, and regular device updating.

Example:

A ,medium-sized manufacturing company believes purchasing cyber insurance means they don't need to invest in regular cybersecurity assessments or employee training. As a result, they fail to implement a regular ,Security Awareness Training program resulting in 4 employees becoming victims of Phishing attacks.

Myth 3 - Cyber Insurance guarantees full recovery from cyber attacks

While cyber insurance can provide financial assistance after a cyber incident, it does not guarantee a full recovery. Recovering from a cyberattack involves various aspects, such as remediation, data restoration, legal fees, public relations efforts, and potential regulatory fines. Cyber insurance may cover some of these costs, but the recovery process can still be complex and time-consuming.

Example:

A small accounting firm suffers a ,ransomware attack that encrypts its client data. They assume their cyber insurance policy will cover all costs associated with recovery, including forensic investigation and data restoration. However, they later discover that their policy only covers a portion of these expenses, leaving them with a significant financial burden and the loss of many weeks of business time while they attempt to restore devices from backups.

Myth 4 - Cyber Insurance Policies are only necessary for large organisations

Small and medium-sized businesses (SMEs) often assume they are not attractive targets for cyberattacks and therefore do not need cyber insurance. However, ,this is a myth. Cybercriminals increasingly target SMEs due to their potential vulnerabilities. Cyber insurance can help mitigate the financial impact of a breach for SMEs and provide resources for recovery.

Example:

A small e-commerce startup believes cyber insurance is primarily designed for giant corporations and doesn't consider purchasing a policy. Unfortunately, they fall victim to a data breach that results in the theft of customer credit card information, leading to costly legal actions and reputational damage. If they had implemented appropriate insurance, these costs could have been mitigated.

Myth 5 - Cyber insurance is too expensive

While the cost of cyber insurance can vary depending on factors like the organisation's size, industry, and coverage limits, it is not necessarily prohibitively expensive. The premiums are often based on an organisation's risk profile and security measures. It is also important to remember that while paying for an appropriate cyber security insurance policy may seem expensive, the cost of data breach fines or recovering from ransomware dwarfs it.

Example:

A small marketing agency assumes that cyber insurance is beyond its budget and chooses not to explore coverage options. Later, they experience a cyber incident where a hacker gains unauthorised access to their client database, resulting in potential lawsuits from clients. The financial impact of the incident proves to be much higher than the cost of a cyber insurance policy, which they could have afforded.

To avoid falling into the above myths surrounding cyber insurance, take the following steps:

- Carefully review the cyber insurance policy, paying attention to coverage limitations, exclusions, and any specific requirements or security measures that must be in place to maintain coverage.

- Recognise that cyber insurance is not a substitute for solid cybersecurity practices. Invest in robust security measures, such as strong passwords, encryption, regular device updates, ,employee training, and ,incident response plans, to reduce the likelihood of a cyber incident and demonstrate a commitment to risk mitigation.

- Assess your ,organisation's cyber risks, considering the industry, data sensitivity, and potential vulnerabilities. This assessment can help determine the appropriate coverage needed and ensure that the policy aligns with the organisation's unique risk profile. Don't forget to implement ,Cyber Security Policies with your staff.

- Small and medium-sized businesses should be aware of their ,attractiveness as cyberattack targets. Recognise the potential impact of a cyber incident on the organisation's finances, reputation, and operations. Consider the affordability of cyber insurance relative to the potential costs of recovery and loss.

- Consult with insurance professionals who specialise in cyber insurance. They can help navigate the complexities of policies, guide suitable coverage options, and assist in understanding the specific risks faced by your organisation.

It is more important than ever for your business to have the right insurance, policies and cyber security plans to stay protected from ,cyber fraud.

To support businesses, we have created a ,Cyber Incident Response Pack containing documents to help keep your business plan for responding to a cyber incident. These documents are designed to complement any existing plans or assist you in creating one.

Contact us today to discuss your cyber insurance or learn more about our affordable ,memberships and ,security services.

https://www.nwcrc.co.uk/post/cyber-insurance-policy

Published: 2023 06 06 11:07:16

Received: 2023 07 03 13:07:47

Feed: North West Cyber Resilience Centre

Source: National Cyber Resilience Centre Group

Category: News

Topic: Cyber Security

Views: 16