Cyber Security News Aggregator

.Cyber Tzar

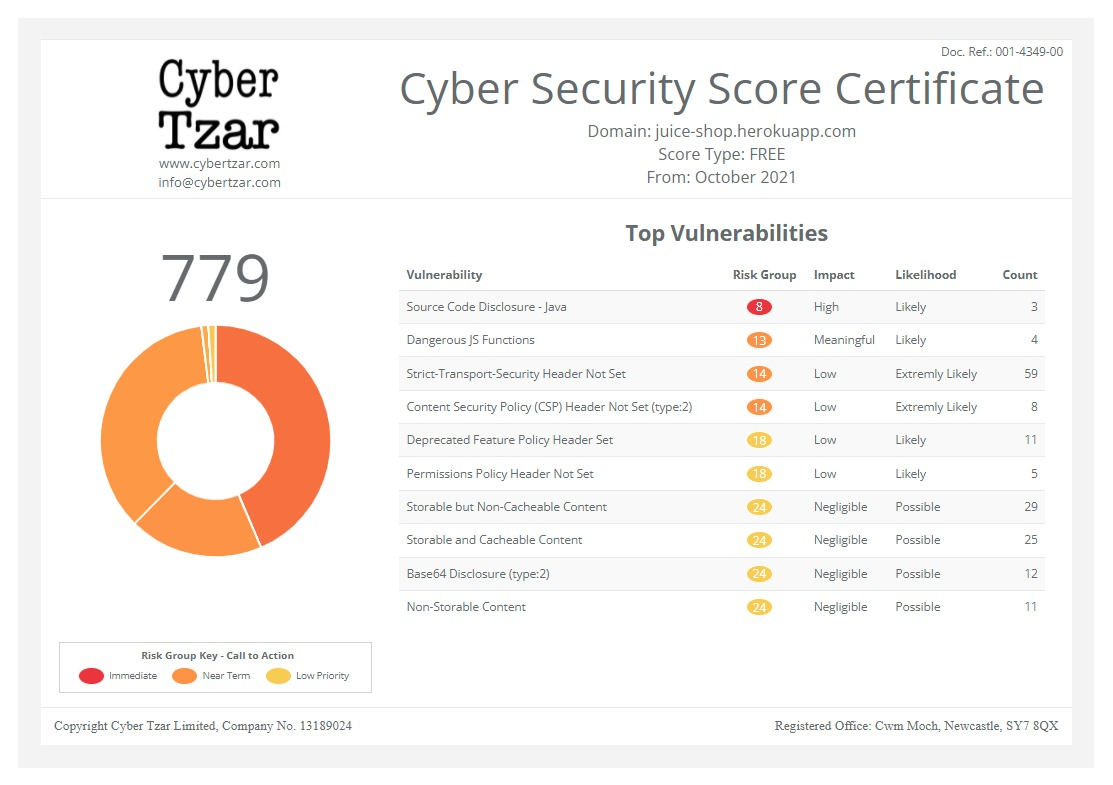

provide acyber security risk management

platform; including automated penetration tests and risk assesments culminating in a "cyber risk score" out of 1,000, just like a credit score.

First slide label

Some representative placeholder content for the first slide.

Second slide label

Some representative placeholder content for the second slide.

Third slide label

Some representative placeholder content for the third slide.

How small businesses can detect, address, and prevent credit card fraud

published on 2024-11-26 16:05:27 UTC by philvilesContent:

Credit card fraud is a growing concern for businesses of all sizes, but it can be especially damaging for small businesses. Here's a comprehensive guide to help small businesses combat this pervasive issue.

Fraudulent transactions can result in financial losses, damaged reputation, and operational disruptions. To safeguard their operations, small businesses must adopt proactive measures to detect, address, and prevent credit card fraud.

Detecting credit card fraud

Early detection of credit card fraud can save businesses from significant losses. Here are some key strategies:

1. Monitor transactions for red flags

Small businesses should be vigilant about transactions that exhibit unusual patterns, such as:

Large or multiple high-value purchases in a short timeframe.

Mismatched billing and shipping addresses/postcodes.

Orders placed with rush shipping requests.

Transactions originating from high-risk countries known for fraud.

2. Leverage fraud detection tools

Many payment processors and Point of Sale (POS) systems include built-in fraud detection features, such as:

Address Verification Service (AVS): Compares the billing address provided by the customer to the one on file with the card issuer.

Card Verification Value (CVV): Requires the three or four-digit security code on the back of the card for online transactions.

AI-Powered Fraud Prevention Tools: These tools analyse customer behavior and flag anomalies in real time.

3. Train staff to spot suspicious activity

Employees should be trained to recognise potential fraud indicators during in-person and over-the-phone transactions, such as:

Customers who appear nervous or distracted.

Cards that are declined repeatedly.

Transactions where the customer refuses to show identification.

Distraction tactics whereby the customer attempts to confuse the employee with noise, actions and peculiar behaviour.

Urgency: if a customer is trying to rush the sale for whatever reason, employees should never skip on protocol for the sake of haste.

Herd mentality: if the customer has brought in an entourage of people who are trying to pre-occupy staff members during a transaction, employees should remain calm and focused on the sale and blank out any human diversion attempts.

Addressing credit card fraud

Once fraud is suspected or confirmed, businesses must act swiftly to mitigate its impact:

1. Decline suspicious transactions

If a transaction raises concerns, it is safer to decline the payment and ask for another form of payment or additional verification, such as a government-issued ID.

2. Report the incident

Notify your payment processor immediately to initiate a fraud investigation. Additionally, file a report with local law enforcement or Action Fraud and share relevant details to aid in tracking fraudulent activities.

3. Engage with affected customers

If fraud affects a legitimate customer, communicate transparently and assist them in resolving the issue, such as by refunding fraudulent charges and providing guidance on reporting the incident to their card issuer.

4. Secure compromised systems

If the fraud stems from a data breach, isolate affected systems, consult cyber security professionals, and notify all impacted parties promptly, including customers and regulatory authorities.

Preventing credit card fraud

Prevention is the most effective strategy for mitigating credit card fraud. Here are measures small businesses can implement:

1. Implement secure payment practices

Use EMV (chip-enabled) card readers to reduce counterfeit card fraud.

Adopt end-to-end encryption and tokenisation to protect sensitive payment data.

Require strong authentication for online transactions, such as multi-factor authentication (MFA).

2. Regularly update security systems

Keep POS software, firewalls, and antivirus programs up to date.

Conduct regular vulnerability assessments and address identified risks promptly.

3. Educate customers

Encourage customers to protect their payment information by:

Using strong, unique passwords for online accounts.

Avoiding public Wi-Fi when making online purchases.

Monitoring their bank statements regularly for unauthorised charges.

4. Establish clear policies

Develop and enforce policies to prevent fraudulent activity, such as requiring ID verification for high-value transactions or suspicious purchases.

5. Partner with reputable payment processors

Choose payment processors that prioritise security and offer advanced fraud prevention tools. Opt for providers with transparent dispute resolution processes to address chargebacks effectively.

Conclusion

Credit card fraud is an evolving threat, but with the right strategies, small businesses can significantly reduce their risk.

By detecting fraudulent activities early, addressing incidents promptly, and implementing robust preventive measures, small businesses can protect their financial health and maintain customer trust.

Investing in fraud prevention might seem costly, but the potential savings in avoided losses and preserved reputation far outweigh the expense. Prioritise security, stay informed about emerging threats, and create a fraud-resistant business environment to thrive in today’s competitive market.

Reporting

Report all Fraud and Cybercrime to Action Fraud by calling 0300 123 2040 or online. Forward suspicious emails to report@phishing.gov.uk. Report SMS scams by forwarding the original message to 7726 (spells SPAM on the keypad).

https://www.emcrc.co.uk/post/how-small-businesses-can-detect-address-and-prevent-credit-card-fraud

Published: 2024 11 26 16:05:27

Received: 2024 11 26 16:25:25

Feed: The Cyber Resilience Centre for the East Midlands

Source: National Cyber Resilience Centre Group

Category: News

Topic: Cyber Security

Views: 16