Cyber Security News Aggregator

.Cyber Tzar

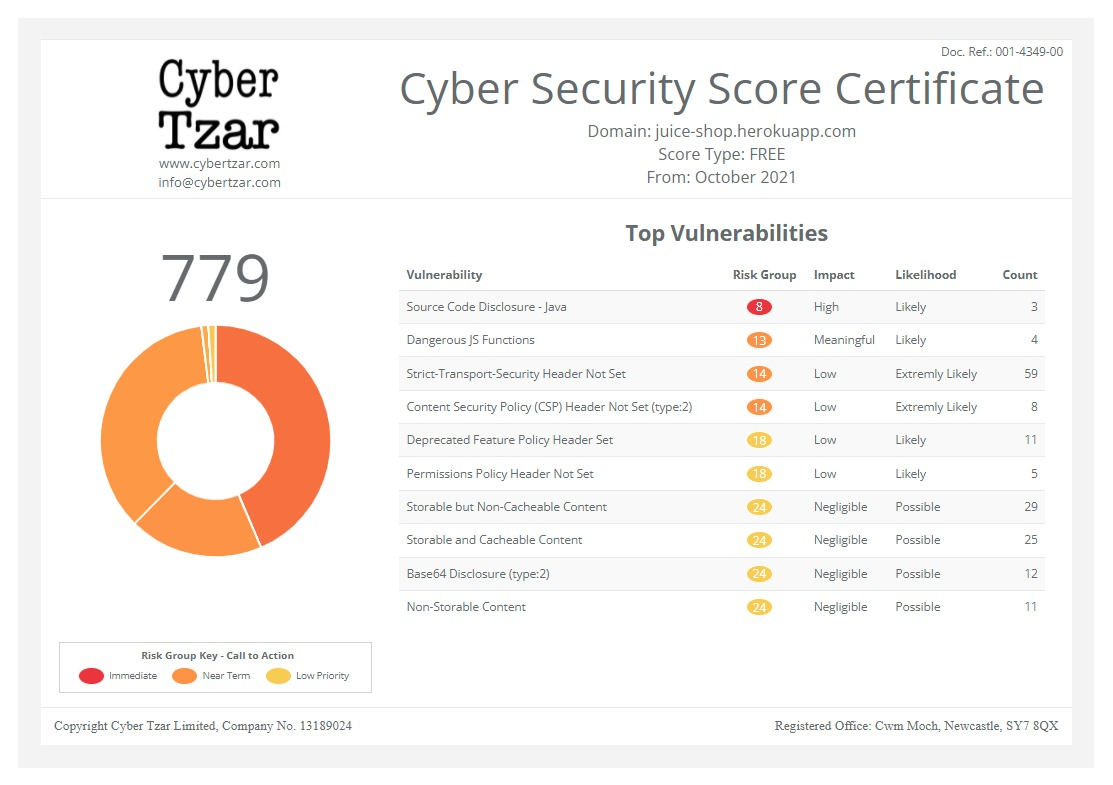

provide acyber security risk management

platform; including automated penetration tests and risk assesments culminating in a "cyber risk score" out of 1,000, just like a credit score.

First slide label

Some representative placeholder content for the first slide.

Second slide label

Some representative placeholder content for the second slide.

Third slide label

Some representative placeholder content for the third slide.

Mobility scooter retailer puts the brakes on potentially fraudulent activity

published on 2024-11-28 20:20:52 UTC by philvilesContent:

In the next instalment of our new ‘Talk of the Town: Cyber Insiders’ feature, a mobile scooter retailer in the Nottinghamshire town of Eastwood tells us how they stopped fraudulent activity in its tracks when they realised that a customer on the phone was not the 'wheel deal'.

For Prime Mobility owner Shah, when he was faced with a customer who wanted to pay £1,700 over the phone for a scooter which they would later collect, alarm bells began to ring when things began to look a little suspicious.

The “customer” tried numerous credit cards to pay for the scooter, which all failed, and because Shah had previously read a cautionary post on Linked In a week before from a trusted source warning clients of a potential dastardly duo operating fraudulently, Shah discovered that something was amiss.

Fraud now affects more people than any other crime in the UK, and it’s not just happening to the big firms. Read our blog on how small businesses can detect, address and prevent credit card fraud.

In this case study, Shah tells us what happened when his staff member Emily received a call that at first didn’t seem suspicious at all, but soon began to resemble something less than ordinary.

So, Shah, tell us what happened...

“I read a Linked In post from the rep of one of our suppliers. It described a man and a woman who were calling businesses like ours pretending to buy scooters and pick them up on the same day. I thought it was interesting to know, but never expected it might affect us.

“Then - I think it was probably a week later - when Emily, who works here, got a call from a lady who seemed to know a lot about scooters. People who visit the shop or call us up don’t usually know a lot about Scooters or what they want, so although that felt odd to Emily, it wasn’t suspect enough to believe anything was wrong at that point. The customer wanted a very specific folding scooter which we didn’t have in stock. So Emily offered her an alternative model priced at £1,700 and the customer said, ‘ok, we'll have that one’.

“Anyway, having agreed to purchase the scooter she said her uncle will be coming in to the shop to collect it later that day so can she pay over the phone. Emily can't authorise payments over the phone; she has to ask me because I do all the payments…so this is where I come in.

“So, I took the call and everything sounded very believable: there was a baby crying in the background, and the customer seemed stressed but also very nice. There were no red flags at this point of the sale, but when I took her card details they didn’t go through.

“I told her it had failed, and she said, ‘oh ok, I’ll use my business card’. So this is the second card we're using now. The first card we tried twice and now the second card isn’t going through either".

Postcode lottery

“I asked her for a postcode and she then gave me two separate postcodes so I thought, ‘ok, this is a bit strange’ and then I remembered what I had read on Linked In about a suspicious male and female calling shops about scooters. She then said she’ll use her mum's card. So now I have three separate card details and three postcodes. And guess what...that card was also declined! I told her it might be a problem with her bank, because sometimes if a customer is spending a large amount of money, the bank will sometimes put a pause on the card for security reasons.

“’It seems like someone might need to approve this’, I told her, 'that could be why it might not be going through'. She then said, ‘ok, I'll go and ring my mum to get approval’. When she came back, she said her mum works for the NHS so she can't pick the phone up. So who did she go and ring? Where did she go?

“At this point I am starting to get really suspicious. She gave me a fourth card - which belonged to her father, apparently. But by now I didn't even bother trying it in the system, but I told her the same: declined. She said, ‘I’ll just ring my dad’. But again, she came back and said the same thing: 'he’s at work, can’t answer the call'”.

A fifth card??!!

“Then she asked if she could use another card...which would have been the fifth! I told her none of these cards are working. She said, ‘I'll give you a call back’. At this point I knew what was going on, and she never called back.

“The thing is she sounded very believable. She sounded really nice on the phone and she had a good reason as to why she wanted to buy the scooter and who it was for. With the baby crying, and her being stressed, it’s kind of believable. But was that just to distract me? Diversion tactics maybe? Was the baby crying even a real baby? The crying stopped after a while. Could it have been audio playing to try and fool me? But after two cards were declined, I began to wonder what was going on. Looking back there was a lot of red flags. Like why would you even have your mum and dad’s credit cards for starters?”.

None shall pass

“So none of her cards worked, they all declined. And she was trying to buy a scooter which cost £1,700.

“I don’t think any of the cards belonged to her or her parents. I believe they were stolen and had blocks on them, and she was just trying her luck. But thankfully they were all declined. I think when she said she was going to ring her parents she was just going to get these extra cards and I think at one point I heard a whisper, so I don't know if she was whispering to someone who's may have been getting these cards ready for her or what, but yeah, a weird one”.

Did you report it to the police?

“Actually, we didn’t. I let the rep (from the Linked In post) know to give him a heads up and to say ‘hey, it happened to us’, but no, we didn’t contact the police on this occasion”.

Has it made you more alert?

“I think so yeah, especially with people ringing up. When someone's in the store, I think you can kind of suss them out. But when it's over the phone it's trickier, and like I said, her story was quite believable to a degree.

“But I think it did put us on edge a little. But it was a good lesson for Emily as well, because she got experience of what looked like someone trying to use fraudulent cards. So, we’re now more switched on when people seem suspicious over the phone”

Shah decided not to contact the police on this occasion. But if this happens to you or your business, reporting mechanisms are in place.

Sharing what you know with the police could be a big help in apprehending the criminals and creating a safer shopping experience for all merchants and consumers.

You can report incidents to the police by using the non-emergency number 101. Your report should include all the information you have. These details can be instrumental in how credit card frauds are caught.

Alternatively, you can also contact Action Fraud. This government agency maintains an online portal that both consumers and businesses can use to report incidents of fraud, which they’ll then pass on to law enforcement agencies for further investigation.

For more information on credit card fraud and how it might affect your business, read our blog here.

If you're reading this as a small business owner and you have a story to tell us, maybe to act as a warning to a similar-sized business, please get in touch. We can share your story with our readers, either anonymously, or with a big shout out to your business.

Cyber crime happens, and becoming a victim of it is nothing to be ashamed of, but it is something that businesses can learn from and ought to know about.

Contact us with your stories or arrange for one of our team to visit you: https://www.emcrc.co.uk/contact-us

Reporting

Report all Fraud and Cybercrime to Action Fraud by calling 0300 123 2040 or online. Forward suspicious emails to report@phishing.gov.uk. Report SMS scams by forwarding the original message to 7726 (spells SPAM on the keypad).

https://www.emcrc.co.uk/post/mobility-scooter-retailer-puts-the-brakes-on-potentially-fraudulent-activity

Published: 2024 11 28 20:20:52

Received: 2024 11 28 20:23:51

Feed: The Cyber Resilience Centre for the East Midlands

Source: National Cyber Resilience Centre Group

Category: News

Topic: Cyber Security

Views: 15